From Separation to Convergence: The History of Public and Private Asset Investing and What Comes Next

A short history of how public funds and private funds moved from strict separation to growing overlap through illiquid buckets, alternative structures, and distribution alliances. Pontoro charts the next step, embedding private market exposure and automated liquidity into a money market style vehicle for retail investors.

Once upon a time, there was a clear delineation between investment vehicles invested in public assets and those invested in private assets. Public asset vehicles, such as mutual funds and ETFs, were for mass distribution, while private asset vehicles, typically in a limited partnership fund structure, were reserved for institutions and very high net worth individuals. Over the past decade, these once separate spaces have been marching inexorably towards convergence. This article discusses the history of how public and private asset investing has been converging and what we at Pontoro believe to be the next evolutionary step towards the further penetration of private markets into the retail investor client base.

Historical Overview

Liquidity Rule

Before 2016, SEC guidance and industry practice limited illiquid assets in mutual funds to 15% of net asset value. This guidance was based on a ’40 Act requirement that mutual fund shareholder redemption requests must be met within 7 days. In 2016, the SEC formally implemented the Liquidity Rule, which effectively codified the 15% guidance into a hard and fast rule. The Liquidity Rule went into effect in 2018 and 2019, with timing for compliance dependent on fund size.

Mutual fund managers tended to use the 15% illiquid bucket to make pre-IPO equity investments in stock funds or to purchase asset-backed debt instruments (e.g., mortgage-backed pools) on a “when-issued” basis for bond funds. For purposes of this discussion, we focus our attention on the inclusion of pre-IPO investments in stock funds. This practice allowed traditional asset managers the ability to back a company through its full lifecycle, including the later stages of its VC rounds. Importantly, it also represented an early intersection of private and public investing, allowing traditional managers to play in the private markets space where they could provide retail investors with limited exposure to illiquid assets. This practice helped pave the way for the next evolution.

Democratization of Alternatives

The next significant advancement arrived with the more recent rise of the “democratization of alternatives,” propelled in large part by Blackstone and a handful of others. As alternative asset managers started to tap out the institutional LP client base, they turned to the HNW and mass affluent segment with new registered fund structures, including tender offer funds, interval funds, BDCs, non-traded REITs, and the operating model propagated by KKR. These funds have been largely successful from a fundraising standpoint, but are not entirely without challenges - most notably, liquidity is intermittent and limited, cash drag impacts fund yields, and FA/investor education can be challenging.

Distribution Alliances

In order to build on momentum and further penetrate the retail client base, alternative asset managers began to turn to traditional managers with their vast distribution networks. Partnerships and acquisitions followed to provide alternative asset managers access to long-tail investors. Recent examples include KKR partnering with Fidelity and Capital Group, Apollo with State Street, Lexington with Franklin Templeton, BlackRock with iCapital, and Blackstone with Vanguard and Wellington Management.

The Next Evolution

We believe the natural progression in public and private assets convergence centers around the ability for private markets to provide efficient and reliable liquidity to retail investors. What better way to achieve this objective than to utilize the immense money market fund universe? Embedding private market assets into what can be termed as an enhanced alpha money market vehicle further evolves the ongoing shift of getting alternative assets into the hands of the retail investor. However, fund composition is not enough. The vehicle must also be structured such that it provides a continuous flow of liquidity by opening up new distribution channels.

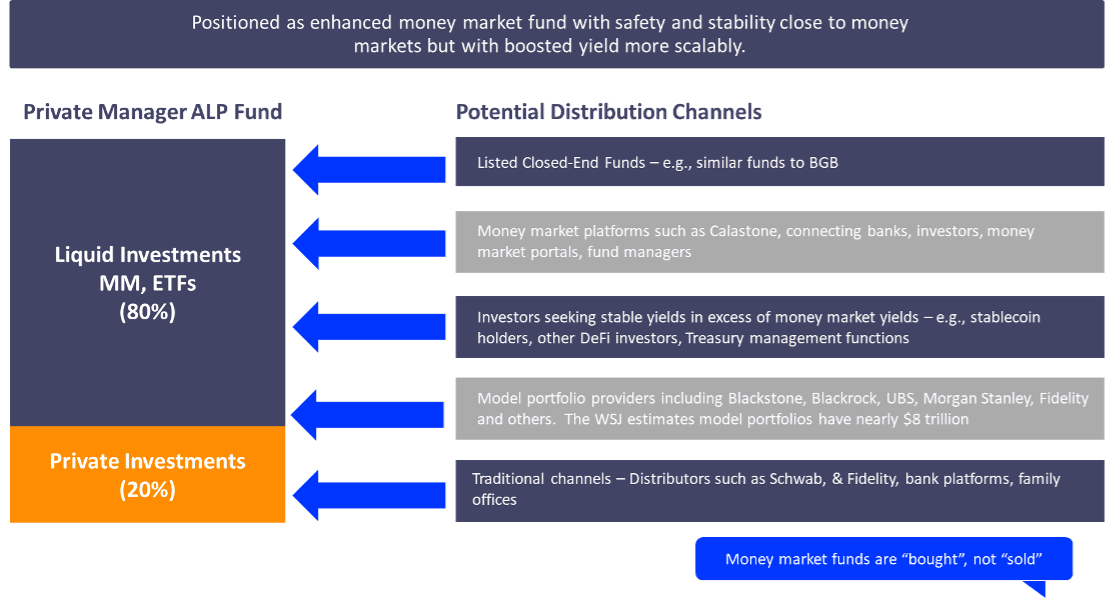

Pontoro has built a unique and patent-pending automated liquidity pool (“ALP”), currently under patent review, that accomplishes just that. Pontoro’s ALP, especially if it is registered as a ’40 Act fund, not only solves the issue of limited liquidity in private markets but can also be marketed as an enhanced money market fund – with the safety and stability of returns that are close to investing purely in a money market fund but with a boost to yield of 200 – 450 basis points as well as access to blue chip institutional asset managers.

In May of this year, SEC Chairman Paul Atkins (Pontoro’s former long-time advisor) noted that the SEC will no longer require retail closed-end funds to limit their investments in private funds to 15% of net assets. We believe it is a small step to broaden the relaxation of the Liquidity Rule to open-ended funds, paving the way for an ALP to become a mutual fund. With total global private wealth estimated at $150 trillion by Bain & Co., such a development would open nearly limitless opportunities.

About Pontoro

Pontoro is a fintech company focused on transforming the private markets by leveraging blockchain technology to bring greater liquidity, efficiency, and transparency. Its patented platform enables the tokenization of LP interests, making more asset classes more accessible through fractional ownership and digital distribution. By building the full tokenization value chain, they are unlocking secondary market liquidity and enhancing price discovery. Pontoro empowers asset managers, fund administrators, and investors to participate more efficiently in the private markets.

Pontoro is pioneering a patent-pending Automated Liquidity Pool (ALP) designed to bridge the liquidity requirements of traditional private funds with the yield-enhancement needs of the DeFi stablecoin market, unlocking substantial economic growth opportunities for both sectors. By pooling stablecoin capital and allocating it across liquid and illiquid assets, the ALP removes the need for 1:1 counterparty matching and uses cash flow-based algorithms to price assets, aiming to offer more efficient liquidity with lower discounts than traditional secondary markets.

For additional information about Pontoro’s liquidity solutions platform and the automated liquidity pool, please visit our website at https://www.pontoro.com/